Florida Home Insurance Too Expensive to Keep? How to Sell Your House for Cash

For a lot of Florida homeowners, the mortgage was never the problem. The insurance was. Premiums in this state run far above the rest of the country, and for some owners the bill, a non-renewal letter, or a roof no company will cover has turned a home they love into one they can no longer afford to keep. If insurance is the reason you are thinking about selling, you are not alone, and you are not out of options. This guide explains why Florida insurance got this expensive, when it becomes a reason to sell, and the fastest way out if that is where you have landed.

Key highlights

- The average Florida home insurance premium is roughly three times the national rate, and coastal homes pay far more, even after some relief arrived in 2026.

- An estimated 15 to 20 percent of Florida homeowners now carry no insurance at all, and those who lose coverage can face force-placed policies that cost far more.

- A home that is hard to insure, often because of an older roof, is hard for a regular buyer to finance, which is why so many sit unsold.

- A cash buyer does not need a mortgage, so the insurance wall that blocks a financed buyer does not block the sale. You sell as-is and pick the closing date.

The short answer

Yes, you can sell a Florida house even when insurance has become the problem, and for many owners it is the cleanest way out. If the premium is more than you can carry, if your policy was non-renewed, or if your roof or a past claim makes the home hard to insure, a traditional sale gets difficult, because a buyer's lender requires insurance to close. A cash buyer removes that wall. There is no mortgage, so there is no insurance requirement standing between you and a closed sale. You sell the home as-is and move on.

Why Florida home insurance is so expensive

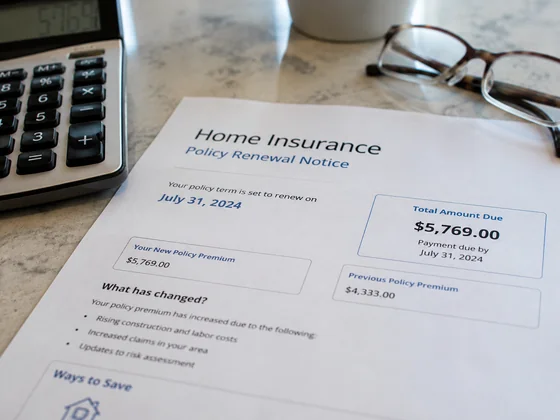

Florida sits squarely in hurricane country, and that one fact drives almost everything about its insurance market. Storms make homes here expensive to insure, and they make it expensive for insurers to buy their own backup coverage, called reinsurance. Add years of heavy claims and lawsuits, and a lot of companies either raised rates hard or left the state altogether. The result is the most expensive homeowners insurance market in the country, with the average Florida premium running around three times the national rate and coastal counties paying the most.

There is some good news in 2026. Reforms and a few calmer storm seasons have brought new insurers into the state, and rates have finally started to ease for many homeowners. But easing is not cheap. Florida is still the costliest place in the nation to insure a home, an estimated 15 to 20 percent of owners carry no coverage at all, and the relief does not reach everyone, especially homes with older roofs or past claims. Officials point to a stabilizing market, while many homeowners say they still feel squeezed, a gap covered well by reporting from CBS Miami.

When insurance is the reason people sell

Insurance pushes people to sell in a few specific ways, and they tend to pile up:

- The premium is simply too high. When the yearly bill climbs past what the budget can hold, the house stops making sense even with the mortgage paid on time.

- The policy was non-renewed or canceled. Losing coverage leaves you exposed, and if there is a mortgage, the lender can step in with force-placed insurance that costs far more.

- The roof is too old to insure. Most Florida insurers will not write a policy on a roof past a certain age, and a full roof replacement is a big bill on a home you may already want to leave.

- A past claim follows the home. Prior storm or water claims can make a property hard to insure at any price, which shrinks the buyers who can close.

The common thread is that all of these make the home hard to insure, and a home that is hard to insure is hard to sell to a buyer who needs a mortgage. That is the trap a lot of Florida owners find themselves in.

Your options

There is no single right answer. It comes down to whether you can absorb the cost, whether the home is insurable at all, and how fast you want it behind you.

- Shop, mitigate, and keep the home. Get new quotes, add wind mitigation, or replace the roof to lower the premium. Best when you want to stay and can fund the upfront work.

- List it on the open market. Put the home up for sale and hope for a buyer who can get it insured and financed. Best when the home is still insurable and you have time to wait.

- Sell it fast for cash. Sell the home as-is to a cash buyer, no insurance or financing to approve, and close quickly. Best when the home is hard to insure or you simply need out.

| Your option | Best when | The trade-off |

|---|---|---|

| Shop, mitigate, and keep | The home is still insurable and you want to stay | Upfront cost for a new roof or mitigation, and no guarantee the premium stays affordable |

| List on the open market | The home can still be insured and financed and you have time | Buyers may not get coverage or a loan, so it can sit for months while costs pile up |

| Sell to a cash buyer | The home is hard to insure, or you need a fast, certain exit | The price is below full retail in exchange for speed and a sale that does not depend on insurance or a lender |

Why a cash sale can be the cleanest exit

When the real obstacle is insurance, a cash buyer solves the exact thing standing in your way. A mortgage is what forces the insurance requirement in the first place. No mortgage means no lender demanding a policy, so a non-renewal, a high premium, an old roof, or a past claim does not stop the sale. The deal rests on the cash, not on whether a company will write coverage.

On top of that, a cash sale removes the rest of the friction. You sell the home exactly as it is, with no roof replacement, no repairs, and no staging. There are no months of showings while the premium keeps draining you. And you pick the closing date, so the sale fits your timeline instead of dragging out. For an owner who needs to be out from under an unaffordable bill, that certainty is the whole point.

What to sort out before you sell

A few things make an insurance-driven sale go smoother when you settle them early:

- Your real numbers. Know your current premium, any non-renewal date, and your mortgage payoff, so you can see what selling actually nets you.

- The roof and claim history. Knowing the roof's age and any past claims helps a buyer make a firm offer fast instead of backing out later.

- Disclosure. Florida requires you to disclose known issues. Being upfront keeps the deal from falling apart at the end.

- Your timeline. If a non-renewal or force-placed policy has a date attached, plan the closing around it so you are out before the costly coverage kicks in.

A cash sale makes most of this easier, because there are no showings to coordinate, no repairs to argue over, and a fixed closing date you can plan around.

Get out from under the insurance bill

Tell us about your Florida house. We make a no-obligation cash offer in 24 hours, buy it as-is even with an old roof or a non-renewal, and close on the date you choose.

Get my cash offer or call (888) 480-5544Selling for cash vs listing with an agent

A traditional listing can work when the home is still easy to insure and you have time to wait for the right buyer. But when insurance is the problem, that is exactly what is missing. A listing means cleaning, staging, and a stream of buyers who keep getting blocked, either because they cannot get the home insured or their lender will not finance it. It can drag on for months, the premium and the mortgage keep running, and agent commissions still come out of whatever equity is left.

A cash sale answers the part that breaks most of these deals: the insurance and the financing. You sell the home as-is, with no roof work or repairs and no commissions cutting into your number, and a good buyer covers the closing costs. You pick the closing date, so the sale fits your situation instead of fighting it. For an owner who mainly wants this off their plate quickly and for certain, that is hard to beat.

Taxes and timing, the quick version

Timing can matter for taxes, so it is worth a quick word with a professional before you sell. When you sell a primary residence, the IRS generally lets you exclude up to $250,000 of gain if you are single, or up to $500,000 for a married couple filing jointly, as long as you meet the ownership and use tests. If the home is a second home or a rental, different rules apply. The details are in IRS Topic 701, but this is the kind of thing to confirm with a tax professional for your situation.

How Sterling Home Offer helps

We buy houses for cash across Florida, including homes that are hard to insure because of an older roof, a past claim, or a policy that was not renewed. We make a real, no-obligation offer based on the actual home and comparable sales nearby, not a lowball guess. Because we pay cash, we do not need the home insured to close, so the problem that blocks a financed buyer does not stop us. We buy as-is, so you replace no roof and fix nothing, and we close on the date you choose. The result is a clean exit from a bill you can no longer carry.

If you want to read more first, our guide on how selling to a cash home buyer works walks through the steps, and what selling as-is really means covers the repairs question. Real seller stories are in our reviews section.

The bottom line

Insurance has quietly become one of the biggest reasons Florida homeowners let go of a house. The premiums are still among the highest in the country, coverage can vanish at renewal, and a home nobody will insure is a home a regular buyer cannot finance. You still have a way out. You can sell a Florida house even when insurance is the problem, and when that is the wall in your way, a cash sale goes straight through it. Get an offer, pick your date, and put the bill behind you.

Florida home insurance FAQs

Why is Florida home insurance so expensive?

Florida sits in the path of hurricanes, which makes it costly to insure and expensive for insurers to buy their own backup coverage called reinsurance. Years of heavy claims and litigation pushed many companies to raise rates or leave the state. Even with some relief in 2026, the average Florida premium is roughly three times the national rate, and coastal homes pay far more.

Can I sell my house if my insurance was non-renewed or canceled?

Yes. Losing coverage does not stop you from selling. It can make a financed sale harder, because a buyer's lender requires insurance to close, and a home that is hard to insure is hard for them to finance. A cash buyer does not need a mortgage, so the insurance problem that blocks a financed buyer does not block the sale.

Does an old roof make my house hard to sell?

In Florida, yes. Most insurers will not write a policy on a roof past a certain age, and without insurance a regular buyer cannot get a mortgage. That is why homes with older roofs often sit on the market. A cash buyer purchases the home as-is, roof and all, so the age of the roof does not kill the deal.

Will I get less for my house because of insurance problems?

Insurance issues can affect price, because they shrink the pool of buyers who can close. But a fair cash offer is based on the actual home and comparable sales, not a lowball guess. You trade full retail price for speed and a sale that does not depend on a buyer getting coverage and financing approved.

How does selling to a cash buyer help with insurance problems?

A cash buyer does not need a mortgage, and a mortgage is what forces the insurance requirement. So a non-renewal, a high premium, an old roof, or a prior claim does not stop a cash sale. You sell as-is, skip the repairs and showings, and pick the closing date, which lets you get out from under a bill you can no longer carry.

This article is general information, not legal, financial, insurance, or tax advice. Florida insurance rules and individual situations vary and change over time. Please talk to a licensed Florida insurance agent, attorney, and tax professional about your specific situation.